How to Stop Collection Calls Legally

Introduction

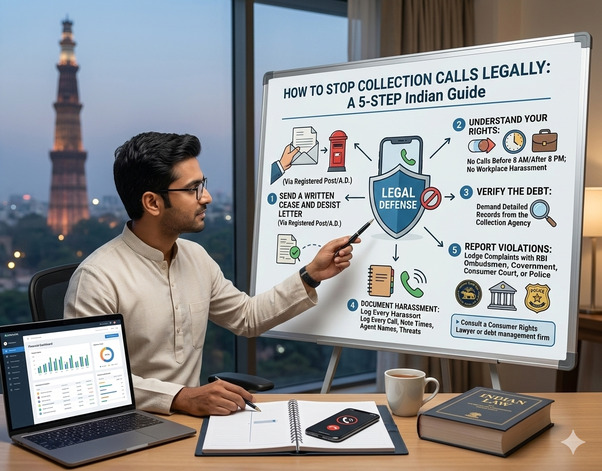

For many borrowers, the most stressful part of debt is not the repayment—it’s the constant collection calls. Aggressive recovery agents often cross the line, turning reminders into harassment. The good news: Indian law and RBI regulations protect borrowers. Here’s how you can stop collection calls legally and regain peace of mind.

What Constitutes Harassment?

Debt collection harassment includes:

- Persistent calls at odd hours.

- Threatening or abusive language.

- Disclosure of debt to family, friends, or colleagues.

- Intimidation or pressure tactics.

Such practices violate RBI’s Fair Practices Code and can be challenged legally.

Step 1: Know Your Rights

- Recovery agents cannot call before 7 AM or after 7 PM.

- They must identify themselves and respect borrower privacy.

- Harassment or intimidation is strictly prohibited under RBI guidelines.

Step 2: Document Everything

- Keep a record of call timings, agent names, and conversation details.

- Save call recordings or screenshots of messages.

- Documentation strengthens your case if you file a complaint.

Step 3: Send a Written Response

- Draft a professional letter/email to the bank stating harassment details.

- Request communication only through formal channels.

- This creates a legal record of your objection.

Step 4: File a Complaint

- Banking Ombudsman: File a complaint against harassment.

- Consumer Court: Challenge wrongful practices.

- Police Complaint: If threats or intimidation occur, lodge an FIR.

Step 5: Explore Debt Resolution

- Negotiate settlements or restructuring with legal support.

- Ensure agreements are documented to prevent future calls.

- Legal strategy transforms panic into power, protecting dignity.

Risks of Ignoring Collection Calls

- Escalation into legal notices.

- Damage to credit score.

- Increased stress and harassment.

Conclusion

Collection calls don’t have to mean harassment. By knowing your rights, documenting evidence, and using legal remedies, borrowers can stop intrusive calls and restore confidence. Debt recovery must be fair, respectful, and compliant—and the law is on your side